Sample Internship Report on Investment Activities of IBBL

This a sample internship report on Analysis of Investment Activities of Islami Bank Bangladesh Limited : A Case Study on Jatrabari Branch Organization: Islami Bank Bangladesh Limited Internship Placement: Dhaka Program: BBA Executive Summary This study has been conducted as a partial fulfillment for BBA program of the department of Business Administration under Bangladesh Islami University. The report will give a...

This a sample internship report on Analysis of Investment Activities of Islami Bank Bangladesh Limited : A Case Study on Jatrabari Branch

Organization: Islami Bank Bangladesh Limited

Internship Placement: Dhaka

Program: BBA

Executive Summary

This study has been conducted as a partial fulfillment for BBA program of the department of Business Administration under Bangladesh Islami University. The report will give a clear idea about the Analysis of Investment Activities of Islami Bank Bangladesh Limited : A Case Study on Jatrabari Branch. I have completed my internship report using of three months internship knowledge. Due to complete the report, I worked Jatrabari Branch in Islami Bank Bangladesh Limited. In this study I have used primary and secondary data.

This report segmented into five chapters, the first chapter is introduction. It will give an idea about how the report is being prepared and background of the study, objective of the study, scope of the study, methodology of the study, time schedule and limitation of the study. In second chapter I have tried to describe detailed description of the Islami Bank Bangladesh Limited. I have mentioned the history, corporate information, vision, mission, core objective, functions, financial information, and SWOT analysis of the IBBL. In chapter three I have tried to describe the theoretical illustration of the topics of the internship that concepts of bank, types of bank, investment banking, types of investment, and important features of investment. In chapter four I have mentioned the theoretical, analytical and computational part of the report mentioning the problems and sort comings. Here I describe analysis and findings on the investment activity, investment sanction activity, and give some significant financial figure of IBBL. In chapter five I have tried to draw the summary of the recommendation the probable remedy to overcome the problems and conclusion.

IBBL does not sanction investment to all sectors equally as they require, rather it concentrates its investments within some limited fields and categories. Its investment procedure is very difficult. Some of the IBBL employers try to violet Islami Shariah when they deal with investment. There has Chance to submit wrong appraisal and evaluation of investment proposal.

IBBL plays a vital role in human resources development and employment generation particularly among the unemployed youths. And also Ensures Shariah compliance through regular and effective guidelines of powerful and highly esteemed Shariah council consisting of thirteen members representing Shariah scalars.

Islami Bank Bangladesh Limited should invest all economic sectors for more profit. It also helps to create new employment opportunity. IBBL should make the investment procedure easy and understandable to attract the potential customer. Official at branch level should more careful in compliance with desired Shariah regarding investment. If employees become well trained, the possibility of wrong appraisal and evaluation of investment proposal will be minimized. Overall I have tried to share my practical learning and experiences in the report that I gathered during my internship period and present it in the perfect and right way.

Chapter-One

Introduction

1.1 Introduction of the Study

The special feature of the investment policy of Islamic Banks is to invest based on profit-loss sharing system in accordance with the tenets and principles of Islamic Shariah. Earning of the profit is not the only motives and objectives of the Islamic Bank’s investment policy rather emphasis is given in attaining social good and in creating employment opportunities. Investment is the action of deploying funds with the intention and expectation that they will earn a positive return for the owner. Funds may invest in either real assets or financial assets. When resources used for, purchasing fixed and current assets in a production process or for a trading purpose, that it can be termed as real investment. Specific examples of financial investments are deposits of money in a bank account, the purchase of Mudaraba savings bonds or stock in a company. Since Islam condemns hoarding savings and a 2.5 percent annual tax (Zakat) imposed on Savings, the owner of excess savings, if he is unable to invest in real assets has no option but to invest his savings in financial assets.

Banking functions of Islami Bank Bangladesh Limited is an important aspect in our economy as it has broken the line of interest based traditional banking system through the introduction Islamic Shariah based banking. Since its commencement in 1983, it has already gained a good reputation in customers as well as the masses of people of Bangladesh. Islamic Banking is especially important in the world countries, which are characterized by unemployment, inequitable distribution of income and wealth, etc. But there are so many constraints in our country in functioning the Islamic banking activities. This paper is an attempt to evaluate the Modes finance of Islamic Bank Bangladesh Limited (IBBL) in terms of productivity and effectiveness. Since it is difficult to measure the productivity of a bank, especially the interest-free Islami Bank Bangladesh Limited, as it does not any visible product. Some specific indicators have been selected for the purpose of measurement of productivity.

1.2 Objectives of the Study

The objectives of the study are

- to analyze the investment activities of Islami Bank Bangladesh Limited;

- to identify factors affecting the investment of Islami Bank Bangladesh Limited; and

- to assess the recovery process of Islami Bank Bangladesh Limited.

1.3 Scope of the Study

This report is limited to the overall descriptions of the bank, its services, investment activities and its position in the industry. This report emphasizes the sequential activities involved in investment activities provide by Islami Bank Bangladesh Limited. At last the general banking position of the bank in the banking industry based on its last couple of year’s performance.

1.4 Methodology of the Study

The study is performed based on the information extracted from different sources collected by using a specific methodology. This report is analytical in nature. The methodology is mentioned bellow:

Data collection : Data were collected from two sources.

- Primary Sources

- Secondary Sources

Primary Sources are

- Face to face discussion with the respective officers and staffs.

- Relevant file study on provided by the officers concerned.

- Face to face discussion with different clients of Islami Bank Bangladesh Limited.

Secondary Sources are

- Annual Reports (2010-2014) of Islami Bank Bangladesh Limited.

- Relevant Text Books, Newspapers and Journals.

- Investment manuals of Islami Bank Bangladesh Limited

- Internet and various studies Report.

- Website of the Islami Bank Bangladesh Limited.

- IBTRA Library.

1.5 Time Schedule of the Study

Objective of the practical orientation program is to have practical exposure for the students. My tenure was for twelve weeks only, which was somehow not sufficient. After working whole day in the office it was very much difficult, if not impossible to study again the Theoretical aspects of banking. On the other hand to prepare my internship report I have faced some limitations as follows. It is a common tendency of any departments to keep back their departmental data and information.

1.6 Limitations of the Study

The present study was not out of limitations. From the beginning to end, the study has been completed sincerely and truthful. But some problem arises from conducting in the study. During the study it was not possible to visit the whole area covered by the banks although the financial statements and other information regarding the study have been covered. Some limitations are given stated below.

v Islamic banking system is different than the traditional banking system

v It is very difficult to analyze this issue without proper knowledge about Islamic banking and economy.

v As it is not conventional so it bears some complexity to understand.

v Some words are in Arabic terms that make it difficult.

v Some information is confidential.

v In many cases up to date information is not published.

v As I am student it is not possible for me to collect all the necessary information.

v I had to complete this report within a very short span of time that was not sufficient for investigation.

Chapter-Two

Profile of Islami Bank Bangladesh Limited

2.1 History and Growth of Islamic Banking Around the World

In the 20th century, the financial and banking world come too acquainted with a new member in the money market known as Islamic Bank with some special features. Islami banking gradually evolved during the last thirty years in some parts of the Muslim world. During 1960’s it was observed that Muslims of Malayasia used to save money primarily for performing Hazz. Such savings mostly kept idle in pillows, under mattresses and floor for avoiding interest, which was unproductive and damaging for the growth and development of economy. For utilizing such saving the Government of Malaysia in 1962 established an interest free financial institution known as “Pilgrims Saving Corporation”. In 1963 Ahmed El Nujjar established a bank at MITGAMAR inegypt by his personal endeavor with a view to bring some development in socio-economic field in the process of Islam. This Mitgram Bank is considered as the Father of Modern Islamic Banking and A.E Niffar is considered as the Father of Islamic Banking System. The tremendous development that the world economy has experienced in the last few decades was contributed by several factors among which, growing institutional supply of loan able funds must have in the human body. Both commercial banks and other development financial institutions provide short, medium, and long-term credits to business persons and entrepreneurs who usually take the lead in ventures of economic development.

Institutional supply of credit has been made possible by a system of financial inter-mediation organized in a way where conventional banks collect small savings from the public by offering them a fixed rate of interest and advancing the loan able funds out of the deposited money to enterprising clients charging relatively higher rates of interest. The margin between these two rates is the banks income. In addition, banks also provide many other services to the public for which it receives service charges. Despite the outstanding contribution of the conventional banking system (interest-based) several ancient and modern economists are critical about its efficiency level. Some economists consider the role of interest in the conventional banking mechanism as a major negative factor that contributes to cyclical fluctuations in the economy (Minsky 1982). More recent concern over the potential instability of the world monetary and financial system was expressed by Maurice Allais, a Noble Laureate in the called for an urgent reform of the World Economic order (Allais 1993, pp13-16). Others vehemently oppose the argument for using rate of interest as a stabilizing tool in the economy (Saud 1980, p. 88). This called for the emergence of a new system of banking capable of tacking new challenges that the present world economy, particularly the financial sector, has been facing. To create a sound economic system all the nations of the world urge to fashion and design their economic lives in accordance with the precepts of Islam. In this regard all the conventional banks are trying to reform their financial structure according to the light of Islam. Now More than 50 Islamic Banks and Islamic institutions have been operating their business all over the world. Besides Muslim countries, Islamic Banks are operating their banking business in non- Muslim countries.

In August 1974, Bangladesh signed the Charter of Islamic Development Bank and committed itself to reorganize its economic and financial system as per Islamic system as per Islamic Shariah. In January 1981, Late President Ziaur Rahman while addressing the 3rd Islamic Summit Conference held at Makkah and Taif suggested, “The Islamic countries should develop a separate banking system of their own in order to facilitate their trade and commerce.” This statement of Late President Ziaur Rahman indicated favorable attitude of the Government of the People’s Republic of Bangladesh towards establishing Islamic banks and financial institutions in the country. Earlier in November 1980, Bangladesh Bank, the country’s Central Bank, sent a representative to study the working of several Islamic banks abroad. In November 1982, a delegation of IDB Bangladesh and showed keen interest to participate in establishing a joint venture Islamic bank in the private sector. They found a lot of work had already been done and Islamic banking was in a ready form of immediate introduction. Two professional bodies Islamic Economics Research Bureau (ERB) and Bangladesh Islamic Bankers’ Association (BIBA) made significant contributions towards introduction of Islamic banking in the country. They came forward to provide training on Islamic banking to top bankers and economists to fill-up the vacuum of leadership for the future Islamic banks in Bangladesh. They also held seminars, symposia and workshops on Islamic economics and banking throughout the country to mobilize public opinion in favor of Islamic banking. At last, in March 1983, the long drawn struggle to establish an Islamic Bank in Bangladesh become a reality and Islami Bank Bangladesh Limited was established; which including - 19 Bangladeshi national, 4 Bangladeshi institutions and 11 banks, Financial institutes and government bodies of the Middle East & Europe including IDB, Two eminent personalities of the kingdom of Saudi Arabia. Later, other four Islamic Banks, Islamic insurance companies and financial institution were established in the country some traditional banks opened Islamic Banking Branches in some major cities. Al-Baraka Bank Limited, called the second Islamic Bank in Bangladesh, commenced banking business as a scheduled bank on May 20, 1987.

Islamic bank is a financial institution that performs; most of the standard banking activities of the basis of profit-loss sharing system conforming the principles of Islami shariah. It operates with the objectives to implement and materialize the economic and financial principles of Islam in the banking area. According to Islami Banking Act 1983 of Malaysia, Islami Bank is a Company which carries on Islami banking business, Islami Banking business means banking business whose aims and operations do not involve any element which is not approved by the religion of Islam”. Islamic Banking is essentially normative concept and could be defined as the conduct of in consonance with the ethos and to the value system of Islam.” Shawki Ismail Shehta viewing the concept from the perspective of an Islamic economy and the prospective role to be played by an Islamic bank there in opines. "It is, therefore, natural and indeed, imperative for an Islamic bank to incorporate in its functions and practices commercial investment and social activities, as an institution designed to promote the civilized mission of an Islamic economy" (lbid) .

Four elements of Islamic Bank

v To avoid Bank interest

v Invest money on profit

v Invest money in Halal business

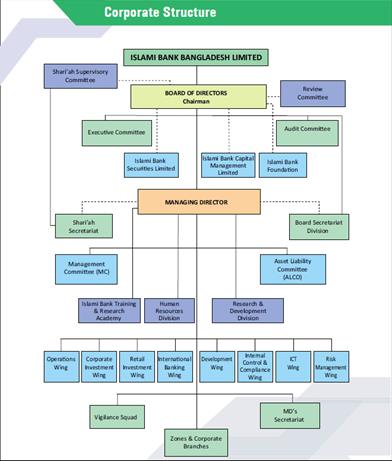

2.2 Structure of the organization

Figure 2.1: Structure of the organization

2.3 Overview of Jatrabari Branch

|

Managing Director |

1 |

|

Executive Vice President |

2 |

|

Vice President |

1 |

|

Senior Vice President |

3 |

|

Senior Principal Officer |

5 |

|

Principal Officer |

6 |

|

Senior Officer |

8 |

|

Junior Officer |

12 |

|

Assistant Officer |

10 |

2.4 Islami Bank Bangladesh Limited at a Glance

2.4.1 Corporate Information

|

Particulars |

Particulars |

|

Date of incorporation |

13March 1983 |

|

Date of receiving Banking License |

28 March 1983 |

|

Date of incorporation of first branch, Local office, Dhaka (formal Head Office, Dhaka) |

30March 1983 |

|

Formal inauguration |

12 August 1983 |

|

Authorized capital |

Tk.20,000.00 Million |

|

Paid Up Capital |

Tk. 12,509.64 Million |

|

Branch Number |

276 |

|

Investment |

Tk. 329,906.00 Million |

|

Share of capital: Local share holders Foreign share holder |

41.43% 58.57% |

|

Deposits |

Tk.335,578.00 Million |

|

Manpower |

12,188 |

|

No. of shareholder |

60,302 |

|

No. of ATM |

1,592 |

|

Zones |

14 |

Table 2.1: Corporate Information

2.4.2 Milestone of Islami Bank Bangladesh Limited

|

Established on |

13th March 1983 |

|

Certificate for commencement of business |

27th March 1983 |

|

Inauguration of 1st Branch |

30th March 1983 |

|

Formal inauguration |

12th August 1983 |

|

Shariah supervisory committee |

1983 |

|

CSR/ foundation activities |

1983 |

|

IPO |

1985 |

|

Listing in DSE Limited |

2nd July 1985 |

|

Listing in CSE Limited |

7th March 1996 |

|

Accommodation of Islami Bank Bangladesh Limited Head Office in its own tower |

10th March 2000 |

|

1st rights share issue |

1989 |

|

2nd rights share issue |

1996 |

|

3rd rights share issue |

2000 |

|

4th rights share issue |

2003 |

|

Opening of 100th branch |

2003 |

|

Opening of 200th branch |

21st June 2009 |

|

Opening of 250th branch |

25th December 2010 |

|

In- house core banking software |

2005 |

|

Islami Bank Bangladesh Limited Mudaraba perpetual bond issue |

25th November 2007 |

|

Inauguration of broker house |

1st January 2008 |

|

Islami Bank Securities Limited |

22nd March 2010 |

|

Islami Bank Capital Management Limited |

1st April 2010 |

|

1st position of Islami Bank Bangladesh Limited in Inward Remittance |

2007, 2008, 2009 & 2010 |

|

100% Branch online banking |

7th January 2011 |

|

Launching of i-banking |

16th December 2011 |

|

Launching of Islami Bank m-Cash |

27th December 2012 |

|

Agreement with CDBL |

29th December 2004 |

Table 2.2 : Milestone of Islami Bank Bangladesh Limited

2.4.3 Board of Directors

The board of director consists of 17 non-executive members. The number of board members is within the maximum limit set by the central bank. The board is composed of experienced members with devised professional experiences. The decision making process and practices are based on free exchange of views to make effective directions for the management which is one of the key responsibilities of the board.

|

Prof. Abu Naser Muhammad Abduz Zaher |

Chairman |

|

Yousuf Abdullah Al- Rajhi |

Vice- Chairman |

|

Engr. Mustafa Anwar |

Vice- Chairman |

|

Abdullah Abdul Aziz Ali Khan |

Director |

|

Engr. Md. Eskander Ali Khan |

Director |

|

Dr. Abdul Hammed Fouad Al Khateeb |

Director |

|

Md. Abul Hossain |

Director |

|

Mohammad Abdullah Al Jalahma |

Director |

|

Mominul Islam Patwary |

Director |

|

Hafizul Islam Miah |

Director |

|

Md. Shahidul Islam |

Director |

|

Mohammad Nazrul Islam |

Director |

|

Md. Abdus Salam, FCA, FCS |

Depositor Director |

|

Humayun Mokhteyar, ACPA, FCA |

Depositor Director |

|

Professor NRM Borhan Uddin, Phd |

Independent Director |

|

Mohammad Abdul Mannan |

Managing Director |

Table 2.3 : Board of Directors

2.5 Objective of the Islami Bank Bangladesh Limited

v To eliminate interest

v To develop human resources for enhancing economic growth and quality of life

v To cover the fulfillment of the basic needs of the people

v The objectives of Islamic banking are not only to earn profit, but to do good and welfare to the people. Islam upholds the concept that money, income and property belong to Allah and this wealth is to be used for the good of the society

v Islamic banks operate on Islamic principles of profit and loss sharing ,strictly avoiding interest, which is the root of all exploitation and is responsible for large-scale inflation and unemployment

v To avoid economic instability

v An Islamic bank is committed to do away with disparity and establish justice in the economy, trade, commerce and industry; build socio-economic infrastructure and create employment opportunities

v To provide safety net for the weak, poor and distressed

2.6 Vision & Mission

- Vision

The vision of Islami Bank Bangladesh Limited is to always strive to achieve superior financial performance, be considered a leading Islamic Bank by reputation and performance.

- To establish and maintain the modern banking techniques, to ensure the soundness and development of the financial system based on Islamic principles and to become the strong and efficient organization with highly motivated professionals, working for the benefit of people, based upon accountability, transparency and integrity in order to ensure stability of financial system.

- Try to encourage savings in the form of direct investment

- Try to encourage investment particularly in projects which are more likely to lead to higher employment.

- Mission

v To established Islamic Banking through the introduction of a welfare oriented banking system and also ensure equity and justice in the field of all economic activities, achieve balanced growth and equitable development through diversified investment operations particularly in the priority sectors and less development areas of the country

v To encourage socio-economic upliftment and financial services to the low-income community particularly in the rural areas.

2.7 Functions of Islami Bank Bangladesh Limited

The functions of Islami Bank Bangladesh Limited are as under:

A) General banking

It includes-

- Mobilization of deposits

- Rreceipts and payment of cash

- Handling transfer transaction

- Operations clearing house

- Maintenance of accounts with Bangladesh Bank and other Banks

- Vollections of checks and bills

- Issue and payment of Demand Draft ,Telegraphic transfer and Payment Order

- Executing customers standing instructions.

- Maintenance of safe deposit lockers

- Maintenance of internal accounts of the bank.

- While doing all the above noted work Islami Bank Bangladesh Limited issue cheque book ,Deposit account

- operating forms, Sscards, cheque book, ledger, cash books Deposit account ledger,

- Preparation statements of accounts and passbook, balance different accounts and calculates profits.

As per Banker’s Almanac (January 2014 edition) published by the Reed Business Information, Windsor Court, England, Islami Bank Bangladesh Limited’s world Bank is 1771 among 3000 banks selected by them. This position was 1902 among 4500 selected banks as on January 1999 edition. Islami Bank Bangladesh Limited’s country Rank is 5 among 29 banks as per ratings made by the above Almanac on the basis of Islami Bank Bangladesh Limited’s Financial Statements of the year 2011

v Preliminary discussion may have with the prospective client regarding his line of business, experience & investment needs

v The past performance of the client to be studied and Branch’s track record of proposed investment

v If the proposal found suitable the client may be asked to submit a formal application along with necessary papers/documents

2.8 Five Years Financial Highlight of Islami Bank Bangladesh Limited

Islami Bank Bangladesh Limited

Balance sheet

As at 31 December 2010-2014 (Amount in Taka)

|

Particulars |

2014 |

2013 |

2012 |

2011 |

2010 |

|

Cash |

6,770,218,585 |

6,636,972,108 |

5,348,163,400 |

5,860,103,625 |

5,002,561,855 |

|

Cash in Hand |

1,550,160,241 |

1,294,274,237 |

1,341,438,945 |

1,585,554,764 |

1,713,064,194 |

|

Balance with Bangladesh Bank and its agent Bank |

5,220,058,344 |

5,342,697,871 |

4,006,724,455 |

4,274,548,861 |

3,289,497,661 |

|

Balance with other Banks and financial institutions |

5,366,014,413 |

5,366,014,413 |

285,958,697 |

350,941,308 |

1,121,909,129 |

|

In Bangladesh |

4,976,518,084 |

33,337,210 |

2,856,213 |

6,930,615 |

800,727,487 |

|

Outside Bangladesh |

389,496,329 |

396,538,734 |

283,102,484 |

344,010,693 |

321,181,642 |

|

Money at call and short notice |

- |

- |

329,700,000 |

29,900,000 |

30,000,000 |

|

Investment |

22,894,749,808 |

18,591,127,858 |

22,502,481,805 |

11,188,289,669 |

14,455,780,134 |

|

Government |

22,735,889,054 |

18,429,298,854 |

18,429,298,854 |

11,091,865,330 |

14,381,918,295 |

|

Others |

158,860,754 |

161,829,004 |

158,412,304 |

96,424,339 |

73,861,839 |

|

Loans and Advances |

54,010,287,476 |

48,672,687,127 |

39,451,355,571 |

37,141,342,619 |

28,477,407,266 |

|

Loans, cash credit, over draft etc. |

49,384,251,667 |

44,372,359,512 |

36,289,189,482 |

33,308,029,435 |

25,298,004,729 |

|

Bills purchased and discount |

4,626,035,809 |

4,300,327,615 |

3,162,166,089 |

3,833,313,184 |

3,179,402,537 |

|

Fixed assets including land, building furniture and fixtures |

2,762,228,892 |

2,798,141,777 |

1,088,418,582

|

1,065,679,827 |

1,013,985,359 |

|

Other Assets |

5,520,848,031 |

4,228,815,180 |

2,840,664,075 |

2,698,386,497 |

2,758,688,987 |

|

Non Banking Assets |

93,580,592 |

94,202,809 |

99,256,359 |

109,688,573 |

|

|

Total Assets |

97,417,927,797 |

81,451,822,803 |

81,451,822,803 |

58,444,332,118 |

52,860,332,730 |

|

LIABILITIES AND CAPITAL |

|

|

|

|

|

|

Borrowings from other Banks, Financial Institutions and Agents |

7,229,331,894 |

206,875,583 |

1,176,417,193 |

225,086,084 |

2,899,505,333 |

|

Deposits and other accounts |

72,152,375,394 |

65,868,030,947 |

59,387,263,182 |

59,387,263,182 |

43,586,356,057 |

|

Mudaraba savings deposits |

183,125,942,453 |

155,191,605,056 |

129,155,650,546 |

109,362,258,451 |

852,123,694,865 |

|

Fixed deposits |

19,969,079,718 |

15,130,072,230 |

14,037,133,261 |

12,164,269,906 |

12,164,269,906 |

|

Other deposits |

1,602,866,184 |

2,126,097,243 |

1,821,156,402 |

1,929,101,150 |

1,276,931,457 |

|

Other liabilities |

8,402,189,838 |

6,766,076,457 |

5,175,368,351 |

3,713,428,714 |

1,276,931,457 |

|

Total Liabilities |

87,783,897,126 |

72,840,982,987 |

65,739,048,726 |

54,755,489,818 |

50,406,775,571 |

v Source : IBBL Annual Report

2.9 SWOT Analysis of IBBL

Every organization is composed of some internal strengths and weaknesses and also has some external opportunities and threats in its whole life cycle.

2.9.1 Strengths

- IBBL provides its customer excellent and consistent quality in every service.

- IBBL is a financially sound company.

- IBBL utilizes state of the art technology to ensure consistent quality and operation.

- IBBL provides its works force an excellent place to work.

- IBBL has already achieved a good-will among the clients.

- IBBL has a research division.

2.9.2 Weaknesses

- IBBL lacks well-trained human resource in some area.

- IBBL lacks aggressive advertising.

- The procedure of credit facility is to long compare to other banks.

- Employees are not motivated in some areas.

2.9.3 Opportunities

- Emergence of E-banking will open more scope for IBBL.

- IBBL can introduce more innovative and modern customer service.

- Many branches can be open in remote location.

- IBBL can recruit experienced, efficient and knowledgeable work force as it offers good working environment.

2.9.4 Threats

- The worldwide trend of mergers and acquisition in financial institutions is causing problem.

- Frequent taka devaluation and foreign exchange rate fluctuation is causing problem.

- Lots of new banks are coming in the scenario with new service.

Chapter-Three

Conceptual Framework

3.1 Definition of Bank

A bank is a financial institution and a financial intermediary that accepts deposit and channels those deposits into leading activities, either directly by loaning or indirectly through capital markets. A bank together customers that have capital deficits and customers with capital surpluses.

Due to their influential status within the financial system and upon national economies, banks are highly regulated in most countries. Most nations have institutionalized a system known as fractional reserve banking in which banks hold only a small reserve of the funds deposited and lend out the rest for profit. They are generally subject to minimum capital requirements based on an international set of capital standards known as the Basel Accords.

3.2 History of Banking Sector of Bangladesh

The formally know State Bank of Pakistan was renamed as Bangladesh Bank right after Bangladesh’s independence. The Bangladesh Bank automatically became official foreign exchange reserve institute. It was too accountable for currency control, monitoring exchange and credit control.

In the early 1970s, the government decided to permit foreign banks to continue their business and nationalize the local banks. In the very decade of 1970s, the primary concern of the government was to develop the country’s agriculture industry. In the mid 1980s, the government adopted new polices for recovery. It didn’t work. Government owned banks continued to fail on recovering the loans. In the 1990s, many private banks started to emerge. Local group of companies became aggressive in investment so the money flow was rather big. Bangladesh bank played key role in managing these private banks with modern outlook. As consciences the banking sectors grow many folds.

3.3 Definition of Conventional Bank

1. “We can define a bank as an institution whose debts are widely accepted in settlement of other peoples’ debt to each other.” -Sayers.

2. “A commercial bank is dealer in capital or more properly a dealer in money. He is intermediate party between the borrower and the lender. He borrows from one party and lends to another and the difference between the terms at which he borrows and those at which he lends from the source of his profit.”- Prof. Gilbert.

3.4 Types of Bank

There are various types of banks. The necessity for the variety among these banks is because each bank is specialized in their own filed. Each bank has its own principles and policies. Different rates of interest are also noted among these banks. All these banks are listed as below :

Savings Bank : These banks are suited for employees with a monthly salary. Low waged people may open an account in the savings bank.

Commercial Bank : These banks collects money from people in various sectors and gives the same as a loan to business men and make profit in in